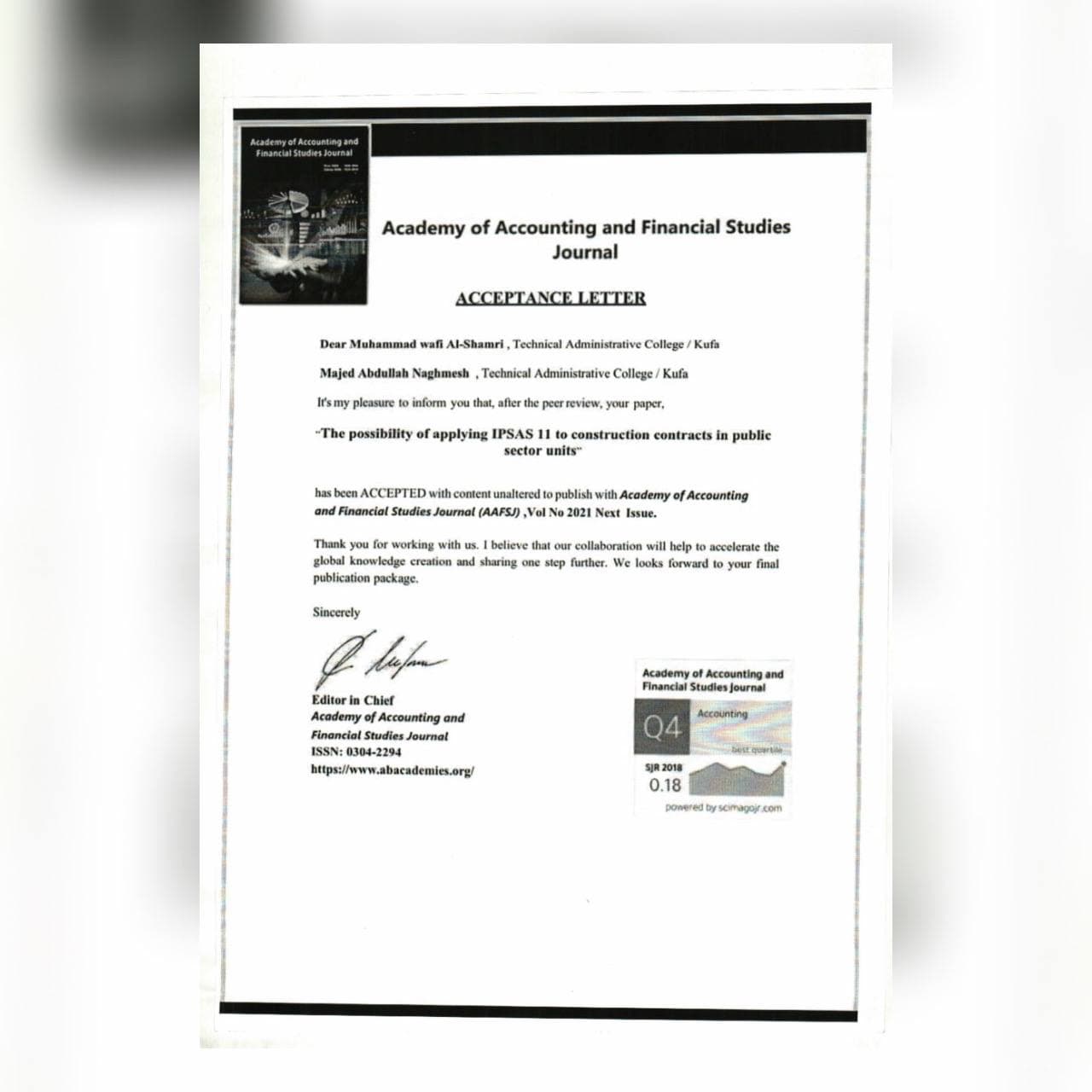

A lecturer from Collage of Administration and Economics /Kerbala University has published a scientific study for The possibility of applying IPSAS 11 to construction contracts in public sector units

in Academy of Accounting and Financial Studies Journal (AAFSJ) ,Vol No 2021.

Dr. mohammed wafi Abd Eawn

Abstract

The research included addressing several problems and difficulties faced by the management of Ashur General Contracting Company, a construction contracting specialist, during the course of its work, such as

overcoming the delay in completing the project for a variety of reasons, including those related to the contractor, as well as the material and professional capabilities.

The reasons for not estimating completion time, as well as the difference between the percentage of technical achievement and the percentage of financial achievement for some projects. In addition to the

problems with measurement and disclosure in the item work in progress, as well as the accounting policies for their calculation, which affect the results of construction companies that deal in construction contracts that this sector suffers from under the amended accounting rule (1).

The research methodology and hypothesis were developed through a review of scientific research in this area. The theoretical side of the research was based on Arabic and English accounting books, accounting

and legal literature, previous studies, and current laws. The study intends to demonstrate how to determine contract revenues, allocate costs, and measure the outcome of its work in Iraqi public sector units using the

current unified accounting system and the International Public Sector Accounting Standard No. (11) and to compare them. The study produced theoretical and applied conclusions that diagnosed the reality of the

company’s current problems.

the firm failed to produce estimates of the projected expenses to execute contracts at the conclusion of the fiscal term. The diversity of accounting policies for measuring the income of the construction sector in

international standards and local rules, as well as the lack of agreement on a unified and optimal method, as each method has its own circumstances, disadvantages, and advantages, made it possible to choose

an accounting method or policy that may not fit the company’s situation and conditions.

Furthermore, the International Public Sector Accounting Standard No. (11) Produced balanced activity results when its specific features were applied to the study sample company’s building contracts utilizing the percentage of completion technique (completion). Whereas the execution of the provisions of local accounting rule No. (1) resulted in imbalanced

activity results, which were reflected by deferring the recognition of

profit (loss) for works completed in a year.